Data Measurement Changes and The Path to Manipulation

Economic data is a direct refelction of how that data is collected and measured. Changing the calculation metrics will produce different endogenous results. As always, I present to you this discussion as a questioning mechanism to look beyond the headlines which are not only based on this potentially misleading data due to measurement issues but then it is extrapolated further to add to the sensationalism and appeal. Therefore, we prefer to delve deeper into information and data and reinterpret it based on more objective analysis.

Let’s begin with a case study of 2008/9 and the mean unemployment duration making it the longest recovery and far worse than the early 1980s stagflationary period. Yes, the 1980s had “higher” unempoyment but no other time period in recent history has exceeded the mean duration of 2008/9. Why? Could measurement issues be a factor? I believe so. Let’s have a look.

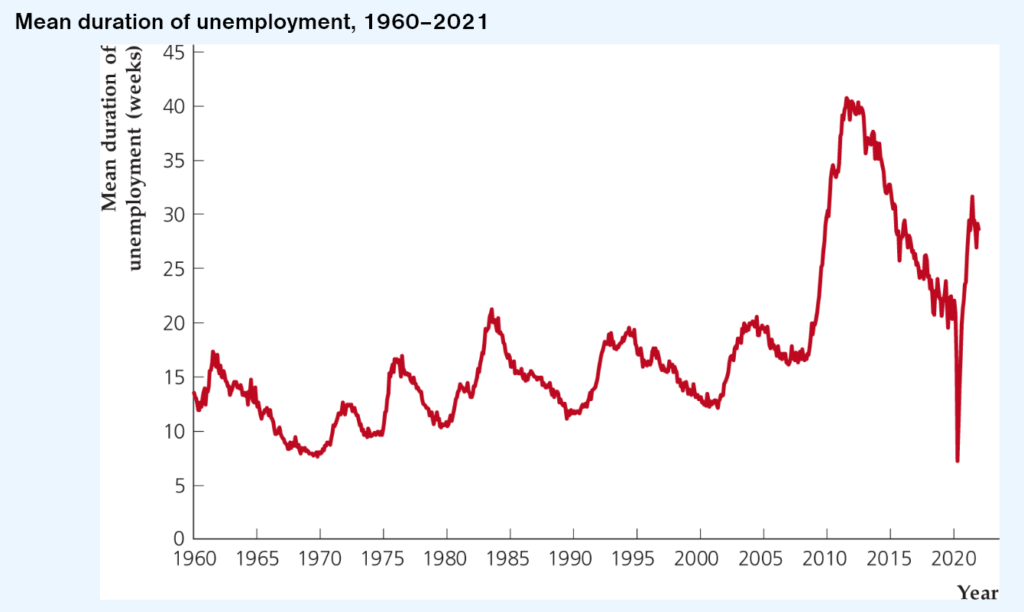

First let’s add some background context. The mean duration of unemployment changes over the business cycle, generally rising during and immediately following recessions and declining after expansions have been underway for a time. One of the biggest differences between the 2007–2009 recession and earlier recessions was the size of the increase in the mean duration of unemployment, which you can see below:

Following the financial crisis and recession of 2007–2009, the mean duration of unemployment rose to a level about twice its typical level. Potential causes of the rise in duration include measurement issues, the extension of unemployment benefits, very large job losses, and a weak economic recovery.

Source: Bureau of Labor Statistics, downloaded from FRED database at fred.stlouisfed.org/series/UEMPMEAN.

Why did unemployment duration rise so high in the 2007–2009 recession and remain so high even after the recession ended? Did anything change in what is used to determine duration of “unemployment” for the household surveys? YES! Were you aware of that? I wasn’t until recently.

Why did this time period exihibit higher duration? Well, there was a change in the survey of households that is used to determine duration. In 2011, the survey was modified to allow respondents to indicate that they have been unemployed for up to 5 years; prior to that, the maximum response allowed on the survey was 117 weeks. Ok, so a change from about 2 years to 5 years. That’s is more than double the time period. Lengthening the time period for respondents to indicate if they have been unemployed for more than double certainly could have impacted the mean duration of the unemployment. What do you think? Per economic studies by several mainstream economists at Federal Reserve Bank of San Francisco – Rob Valletta and Katherine Kuang, this change “progbably” raised the mean duration meaasure by about 3 weeks. That is all? I think more! We don’t need to quantify just add some healthy skepticism here and question it as it logically does not make sense.

A second reason for the rise in unemployment duration was the extension of unemployment benefits. Unemployed people were eligible to receive unemployment benefits for up to 99 weeks during and after the 2007–2009 recession; usually they are limited to receiving benefits for at most 26 weeks. Ok, once again, they have changed the measurement. Benefits extended from 26 to 99 weeks so almost 4x longer. That should sway things significantly. This extension of benefits may have led some unemployed people to wait longer for a better job than might have otherwise been the case. Therefore, some/many/most unemployed people remained unemployed collecting benefits for 4x longer directly affecting the rise in mean duration of unemployment. Per Fed Reserve Bank of Chicago estimates – Aaronson, Mazumder, Schechter, they believe that the extension of unemployment benefits may have raised the mean duration of unemployment by 3 to 6 weeks. So raising benefits for 73 more weeks only raised mean duration by 3-6 weeks? Once again, I would think higher.

So with both above, mainstream economists brushed off measurement issues as only accounting for 6-9 weeks of added duration so the remainder is “most likely” due to macroeconomic (cyclical) factors. Yes, there were certainly several key economics factors contributing to this long recovery such as significant decline in wealth both from housing and financial assets which further impacted consumers’ demand for goods, housing, and financial services. However, the point here is why was this mean duration of unemployment much LONGER than other recessions? The change in measurement is most likely the main culprit but the headlines wouldn’t tell you that although it would make a great story exposing possible data manipulation to help political and legislative agendas.

History repeats. Economic, business, and market cycles all repeat as they are based on humans and their emotions and behaviors. They tend to play out in a similar fashion. And this time period is no different. We are in for a slower cycle that recent past as there was too much money created so it needs time to work throught the system. Although real wages haven’t grown much in many sectors, nominal wage growth was significant and fueling the services and goods consumption.

Now with much higher rates and higher cost of money, we are experiencing a rerate of risk. Asset prices set to come down from their “bubble” state. Many businesses that rely on constant refinance will face greater hardships at these signficantly higher rates. Raising over 500 bps in a ltitle over a year has its negative effects as we see with the liquidity and duration risk at the banks. Smaller banks even more affected. Banks lending standards are getting stricter causing lower supply of loans which is coupled with lower demand for loans. Liquidity and remain liquid are key in a time period of tighening liquidity.

Bottom line: There is hope for the future, however, we will likely have some bumps ahead. Always question the headlines and news and search for the truth.

Sign up for our newsletter and subscribe to The RO Show to stay ahead of all the latest in money, economics, investing, business, and more!